When you’re in your 20s, does the concept of your ‘net worth’ even cross your mind? Most of us don’t even know how to manage our personal finances properly during this time, or we’re probably just getting started – and that’s okay. Your 20s are one of the most exciting at rough periods in your life – you’ve just finished college, and you’re figuring out how to make it work while juggling multiple things at once. You’re working your first (or second) job, living alone, managing your health, and trying to make sense of the various expenses you suddenly have. All of this can get pretty overwhelming, which is why it may take you considerable time before you become financially responsible and start thinking about building your net worth. Your net worth is simply what’s left after you subtract the value of all your liabilities from your assets. The earlier you start working on your net worth, the better it will be for you in the long run. In this article, we’re going to talk about five things that threaten your net worth:

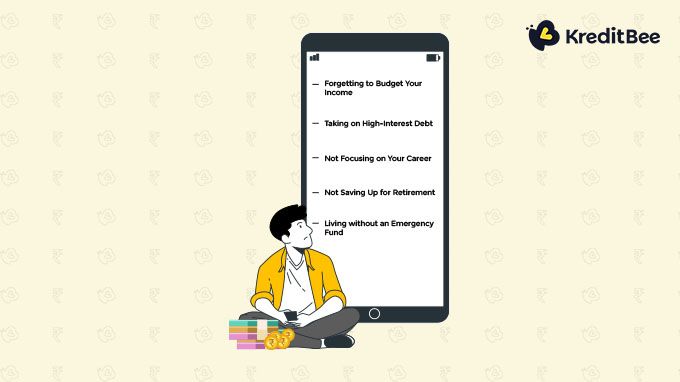

1.Forgetting to Budget Your Income

Most people groan when they think about creating a budget, because it limits the amount of money they can spend. While it’s true that creating and abiding by your monthly budget can be hard (and very annoying at times), it’s an essential tool that you need if you want to save anything at all. That’s what a budget is supposed to help you with – it’s supposed to help you save a considerable sum of money every month without making you compromise on your needs and wants. And how does it do that? By tracking every rupee that you earn. Once you build a habit of tracking your expenses (small personal loan EMIs, credit card bills) and income (monthly salary, freelance income), you'll know where your money is going. This information will help you cut down on unnecessary spending and save. The more you save, the higher your net worth will be.

📗 Related Blog- 4 Extremely Easy Ways You Can Lose Money

2.Taking on High-Interest Debt

This is another mistake we’re all prone to making in our 20s. While we’re all trying our best to manage our money effectively, some of us end up taking high-interest debt without even realising it. Common examples include a credit card, small personal loans, and education loans. Most of you will graduate with an education loan, which you’ll spend the first three-four years paying off. While it’s not something you can entirely avoid, a credit card and unsecured personal loan totally are. You need to know that credit cards are a very expensive way to borrow money, as they carry an average interest APR of 40%. If you don’t pay credit card bills fully on the due date, you’ll get trapped in high-interest debt. The same goes for a small loan – avail of one only when it’s the only option left for you.

3.Not Focusing on Your Career

All of us want to have a well-paying job doing something we love. But not everybody is this lucky. If you're stuck in a job you don't enjoy, figure out how to make the switch to your desired industry. Finding yourself a good mentor who will help you is a good idea. Once you get a job you're good at, it won't feel like work, and you'll be a natural at it. In time, your efforts will get noticed, and the money (increments, bonuses, promotions) will start trickling in. If you're already working in your preferred industry but aren't earning well enough, you could work on upgrading your skills by taking short courses for the same. Doing so will help you bag better jobs and better companies. If you're short of cash, a small personal loan could help with that. Whatever the problem is, work towards the solution, even if you’re lost and don’t know what to do.

4.Not Saving Up for Retirement

Most of us feel that a monthly contribution towards our PPF (Public Provident Fund) or EPF (Employees' Provident Fund) accounts will suffice. You couldn't be farther from the truth. You need to invest your hard-earned income in high-yield assets so that you have a substantial retirement corpus for yourself. Most of us also fail to correctly estimate how big our retirement corpus needs to be because we underestimate how high inflation will be by the time we retire. If needed, you can also take help from a financial planner to help build your retirement corpus efficiently.

5.Living Without an Emergency Fund

Ever since you can remember, your parents have always emphasized the importance of saving for a ‘rainy day’. They’re absolutely right, because you can never predict when an emergency will befall you. And when it does, having adequate money to overcome it can be life-saving. You should always try your best to stay away from debt. There’s nothing wrong with availing of small personal loans, but that should ideally be your last option. This is why we always recommend creating and building an emergency fund worth 3-6 months of your salary. This way, you’ll always be prepared for an emergency and avoid debt.

📗 Related Blog- 4 Proven Habits for Financial Stability

In Conclusion

Unless you come into a fabulous amount of wealth in your 20s, your net worth won’t really improve if you’re not doing anything to boost it. The points mentioned above are tips you can start with. Remember – always save as much as you can, and take out a loan only if it’s an emergency. When you need small personal loans, you can always turn to KreditBee. It is India’s leading personal loan platform that offers quick loans online. To get more information on how you can avail of a personal loan, email us at [email protected], and we will take it from there.

AUTHOR

KreditBee As a market leader in the Fintech industry, we strive to bring you the best information to help you manage finances better. These blogs aim to make complicated monetary matters a whole lot simpler.